Resource Wars in The Middle East – the question is when

THE MATTERHORN INTERVIEW – February/March 2013: Hossein Askari

“The Middle East will blow up – the only question is when”

In this exclusive interview, the renowned economist and energy expert Hossein Askari reflects on some crucial topics of our time, inter alia: current developments in the energy business; the high oil price and the main drivers of it; the Iranian conflict and other challenges in the Middle East; China as the rising energy power; gold-for-oil trading; and Islamic Finance.

By Lars Schall

Hossein Askari, who was born in Iran and went to the UK at the age of nine to receive his schooling, earned his Ph.D. in Economics at the Massachusetts Institute of Technology (MIT). Since 1982 he has worked at George Washington University, where he has served as Chairman of the International Business Department and as Director of the Institute of Global Management and Research and is now Iran Professor of International Business and International Affairs.

Hossein Askari, who was born in Iran and went to the UK at the age of nine to receive his schooling, earned his Ph.D. in Economics at the Massachusetts Institute of Technology (MIT). Since 1982 he has worked at George Washington University, where he has served as Chairman of the International Business Department and as Director of the Institute of Global Management and Research and is now Iran Professor of International Business and International Affairs.

Askari has written extensively on economic development in the Middle East, international trade and finance, agri-business and oil economics, including twenty books, six monographs and over one hundred refereed journal articles. His latest book is “Conflicts and Wars: Their Fallout and Prevention” (Palgrave Macmillan, July 2012) with another forthcoming entitled “Collaborative Colonialism: The Political Economy of Oil in the Persian Gulf” (Palgrave Macmillan, 2013). His opinion pieces have been published in the New York Times, Washington Post, International Herald Tribune, The Christian Science Monitor, US News and World Report, Foreign Policy and in other newspapers and websites. Moreover, he is a regular contributor to Asia Times Online.

Lars Schall: Professor Askari, are “resource wars” just a phenomenon of modern times or isn’t that something that we see more or less at work throughout history?

Hossein Askari: Historically, resources have been the fuel of colonialism. The colonialist-imperialist powers were after resources from around the world, as they are today. What is different today is that the colonialists are collaborating with despots around the world to get what they want. They support these despots to stay in power. The despots and their cronies enrich themselves. And the colonialist powers get what they want–resources, exports of arms to these countries with their companies and influential officials profiting in the process. All of this at the expense of the citizens of the exploited countries. This is what I call collaborative colonialism in my forthcoming book.

L.S.: To have the control of energy flows is extremely crucial in our time. Which conflicts do you see as “resource wars” that are connected to energy?

H.A.: To my mind, US support of oppressive dictators in the Middle East and Africa are an integral part of the resource wars. China is now stepping in in a big way around the world. I think that the US is very shortsighted. The Middle East, especially the Persian Gulf, will blow up. The only question is when? Instead, the US should use tough love and help these despots to change as the only way forward–fundamental political, social and economic reforms. There is no other way.

L.S.: Is the control over the supply of energy resources for the economy ultimately the predominant factor for the whole social life?

H.A.: Yes, energy is crucial for modern life but I don’t think that it will be oil that matters in 50 or so years. We will need cleaner fuels–natural gas and renewables.

L.S.: I think that an expression of the importance of energy is manifest in the traditional relations between international banks and the major oil companies. Why is it that they seem to have been in a symbiotic relationship with each other for more than a hundred years? To be honest, to me it looks kind of incestuous the way that these oil and financial relationships are all intertwined.

H.A.: Access to finance has been traditionally important in the oil and energy business. Some of these energy projects require massive financing in production and transportation (pipelines and tankers). In the 1940-1970 period, Middle East rulers borrowed from Western institutions to finance their lifestyles and keep their countries afloat. In more recent times, the rich rulers of the Middle East have also parked their ill-gotten gains in Western financial institution.

L.S.: Now that we talk about banking and finance, let us raise the topic of how monetary policies have an impact on oil prices. Can you explain to us the connection, please?

H.A.: To my mind, the main drivers of oil prices have been global GDP growth and supply disruptions. So by affecting economic growth, monetary policy definitely impacts oil prices. Moreover, given that oil is priced in dollars, a depreciation of the dollar will lead to adjustment in oil prices in dollars and in other currencies.

L.S.: What are the main drivers for the current oil price? Why is it so high?

H.A.: Besides the basic forces of supply and demand, a number of other factors have also been proposed as important price determinants:

(i) The role of monetary policy (particularly that of the U.S. Federal Reserve), as the central bank prints more money, the demand for goods rises. Knowing that money is depreciating at a fast rate, consumers and producers become speculators and develop high inflationary expectations. Producers withhold commodities in order to take advantage of higher prices around the corner, while consumers rush to buy and store commodities in anticipation of price increases. In the case of oil, though, the ability of producers to withhold supplies and consumers to hoard is somewhat constrained. For producers, high storage costs, potential loss of long-term clients, and damage to oil fields in the event of shutdowns all pose potential problems in saving oil for a higher future price. For consumers to hoard oil, they incur a significant storage cost and near-impossible logistical challenges.

(ii) The role of speculation, as speculation in the futures markets could increase price volatility, but not long-term prices. If a speculator buys an oil-futures contract, the purchase adds to the demand for oil. But if the speculator does not take delivery and sells back the futures contract before maturity, then there is no net addition to demand.

(iii) The value of the U.S. dollar (impacted, by the aforementioned Federal Reserve policymaking), as it reduces the real price of a barrel of oil for producers. But the currency is simply the unit of account; although prices are quoted in dollars, in the end it makes no real difference how oil is priced—dollars, euros, pounds, or yens (domestically, of course, the price of oil may go up or down and by differing amounts in differing currencies because of exchange range movements.) Oil is a global commodity, with prices roughly the same the world over after accounting for any differences due to transportation cost and taxes. If oil priced in dollars suddenly becomes slightly less expensive due to exchange rate fluctuations, the demand stemming from London or Tokyo will rapidly restore the price to equilibrium levels. In short, it is difficult to establish a direct one-to-one causal relationship between the value of the dollar and oil prices.

The most recent (dollar) price peak was in large part driven by a rapidly growing world economy, a depreciating dollar, and especially confrontation with Iran and conflicts in the Middle East, especially Iraq. While the price of oil, like that of any other commodity, is driven by supply and demand, it would appear that conflicts and upheavals leading to sudden supply disruptions have played the most significant role in the wide price (in real terms) gyrations during 2001-2011. No major spike exists without a corresponding conflict, and vice-versa.

L.S.: Is there an oil price above which you would say it becomes extremely difficult for the economy bear it?

H.A.: I don’t believe that there are any such red lines in economics. Higher oil prices have some positive effects (for those in the oil business) and largely negative macroeconomic effects. But these are discrete effects. Also, the impact would be very different if oil prices rise gradually to a “very high” level as opposed to rising to the same very high level overnight. We have clearly adapted to the longest period of high oil prices ($80-$100) without too much problem. Could we have done the same if oil prices were in the $100-$120 range? Probably say. What if in the range of $150-$200? I don’t know. What if in the range of $300-$400? I think that then the pain might be unbearable.

Please also remember that all these prices are assumed in 2013 dollars because if oil prices took a dramatic jump, global inflation would increase, and real oil prices would in turn decline.

L.S.: How important are the option markets for the pricing of oil?

H.A.: I think that the option market is important to the extent that it is another indicator of oil prices–namely, you can deduce the implied price from options– and it is helpful in completing the market and affording arbitrageurs, hedgers and speculators an important vehicle for pursing their business.

L.S.: A huge factor in the energy market is the United States of America. Do you believe that the shale oil and gas boom will lead to energy independence for the U.S.? And what do you think about the report that was released at the end of last year by the International Energy Agency (IEA) that said that the United States will soon become the biggest oil producer in the world?

L.S.: A huge factor in the energy market is the United States of America. Do you believe that the shale oil and gas boom will lead to energy independence for the U.S.? And what do you think about the report that was released at the end of last year by the International Energy Agency (IEA) that said that the United States will soon become the biggest oil producer in the world?

H.A.: For the last 3-4 years I have said that shale oil and especially gas will transform the global energy industry. The reasons are simple: Shale gas will be found in abundance around the world (not just in the US), the sources of this gas is more diverse and closer to the market, Shale oil deposits in north America in my view parallel conventional oil deposits of the Persian Gulf (yes, they are more costly to produce) and are economically competitive at prevailing oil prices.

As to US oil production, let me start out by saying that the US is already a big producer of oil. I believe that it is third, after Russia and Saudi Arabia. But the US is also a big importer of crude oil. So yes, with more reliance on gas and higher shale oil output, the US will import less oil but will it become the largest producer, yes maybe (and by the way not a big exporter ever in the foreseeable future).

I think that the IEA Report is an excellent document. I agree with all of its broad predictions but the details and the exact timing of developments could prove to be somewhat different.

L.S.: What kind of impact would this have on the relations of the U.S. towards the Middle East?

H.A.: I think that the US footprint in the Middle East will decline more rapidly because of these developments. It will be imperative for oppressive rulers in the Persian Gulf to embrace fundamental political and economic reforms now while they have time and more financial leeway. If they don’t, they will be deep trouble with conflicts and uprisings that could mirror Syria as the US has increasingly less interest in shedding blood and treasure to support them. In short, I believe that the US will slowly, but surely, lose interest in the Persian Gulf and its problems. And this may encourage more protests in the region but also it will take the cork out of the bottle and enable more comprehensive reforms in the region.

L.S.: Let’s turn to Iran. You believe that the Iranian regime is not Islamic at all. Why do you think so?

H.A.: Let me correct you, I don’t think that any of the Muslim countries of the Middle East are Islamic. The Islam of the Quran and of the life of the Prophet Mohammad has some important political, social and economic principles.

First, The Unity of Creation is of paramount importance. To kill (torture, imprison, etc.) one innocent person is akin to killing (torturing, imprisoning, etc.) all humankind.

Second, God gave the world the environment and natural resources to humankind in TRUST to share equitably today and WITH all future generations. Oil does not belong to rulers! It belongs equally to all citizens. It must be managed in such a way that all future generations receive similar benefits. Now, let’s be serious. Do these rulers live like their average citizens? No, they are living lavishly at the expense of this and future generations.

Third, rulers are supposed to be selected by their communities. Tell me which ruler is freely selected? Rulers are expected to seek advice and criticism. Tell me which ruler even tolerates criticisms? The Prophet Mohammad is reputed to have lived modestly and said that rulers should live as their poorest citizens so that they would experience poverty and eradicate it.

Fourth, and possibly most important, at the core of an Islamic society there must be social and economic justice. Corruption is absolutely admonished. Tell me which of these countries is just? To me New Zealand, Sweden, Norway, Finland and the like practice Islamic doctrines more than do these Middle East Muslim countries.

If these countries really practiced the Islam of the Quran and the life of the Prophet Mohammad, the rulers would acknowledge that the oil and gas reserves belonged to the citizens of this and future generations. It would be managed so. And the rulers would have no special access to these revenues. Surely rulers could not object to this? And surely the US could persuade its oppressive rulers to behave so!

I could write a book about this. But I will stop here. Enough said.

L.S.: Okay, but if the Iranian regime is indeed not Islamic but is perceived as such, isn’t then something very wrong right from the beginning in international relations vis-à-vis Iran?

H.A.: Again, I believe that the term “Islamist” is the most misused label today. It is used by all to justify what they want. Those that are today generally labeled as Islamist profess Islam but do not practice the Islam of the Quran and of the Prophet. They are largely terrorists that use Islam for their own ends. The West uses the term Islamist to label its enemies who are Muslims but ironically who don’t follow the Quran. Despotic rulers also use the label to frighten the West and get support for their dictatorial rule. It is a very unfortunate state of affairs. The world is being divided along false religious lines.

L.S.: Is the problem with Iran really about the nuclear program, or isn’t that more or less a narrative for complete dis-informed idiots that don’t have any clue of the facts? (1)

H.A.: No, the regime is the problem for the West and Israel. Under the Shah, they were happy to see Iran get heavy and light water reactors. But not now. The West wants a regime change.

From the Iranian perspective, I believe that the clerics and Iranians do not feel safe with heavily armed Arabs in the Persian Gulf, US forces all around and with the memories of the Iran-Iraq War –the US and the rest of the West supplying Iraq with internationally outlawed chemical weapons. Do you really expect the Iranians to trust what the West professes? Iran wants security. The nuclear program is the only way. This is the price of Western duplicity. I am sure that no matter what Iran says and signs, they will want to master the nuclear fuel cycle to be a month away from having the bomb if needed. Frankly, I would if I were in their place and after what they have gone through.

L.S.: In the past you were optimistic that a collapse of Iran’s currency, the rial, would lead to regime change. Do you still think so?

H.A.: I have always said that it is tough to get the policy changes you want from sanctions, especially if they are not multilateral.

First, and foremost, it must be a policy that the people of the country also want changed. That is not the case here. Iranians want the country to master the fuel cycle and be like Japan, that is one month away from making a bomb if needed.

Second, sanctions must cause direct pain on regime insiders (in this case on the Revolutionary Guards and on business backers of the regime) or so much pain on the general public that they protest. That is not yet the case here. Sadly, innocent people are suffering and the sanctions are not causing enough pain on regime insiders.

L.S.: Can you explain to us the way Iran is conducting its oil business under the sanctions?

H.A.: Iranians have been clever with getting around sanctions. In the past banks used the Iranian central bank and foreign central banks. Now they get paid in gold. They do barter deals, they go through third countries to import what they need. They give discounts on their oil. All this effectively reduces the purchasing power of their oil exports.

L.S.: I would like to ask about another motive to put Iran into the corner, which has to do with an oil price above or around $80 per barrel. I think the Gulf states have an interest in keeping oil prices high enough in order to balance their own budgets at a time of increased social spending and other measures that are used to isolate these regimes from the effects of the Arab Spring. These regimes need crude oil prices of about $ 80 per barrel to keep their finances in order. Which in turn means that Saudi Arabia and others have an interest in keeping Iran in the corner; that way Iran cannot attract foreign companies to rebuild the infrastructure of its oil and gas fields and expand it. On the other hand if the current sanctions would be lifted and energy companies could operate freely in Iran, then its oil and gas production would boom, which would increase the total supply — and consequently the world price would fall. Is this totally out of touch with reality?

H.A.: Let me first respond by agreeing with you that other Persian Gulf countries (not so much the very high per capita rich countries of Qatar, the UAE and Kuwait), especially Saudi Arabia, need an $80 price for a barrel of oil. In the six GCC countries, the unwritten contract is simple. We, the rulers, rule and we provide you with decent material comforts. We, the rulers, take what we want and support you. This Saudi Arabia had a hard time doing in the period 1983-2000. It is a contract and policy that is not sustainable for a number of reasons. Government expenditures will eventually exceed oil revenues. People will eventually resent the lavish lifestyles of corrupt rulers and their cronies in comparison to their own. And eventually people will want political and personal freedoms even if materially satisfied, but especially if inequities and economic hardships.

L.S.: What is OPEC thinking about the 40 year plus debasement of the dollar in general and how are they defending themselves?

L.S.: What is OPEC thinking about the 40 year plus debasement of the dollar in general and how are they defending themselves?

H.A.: In my opinion, OPEC countries do not think of the long run. They are focused on the near term and for that all that matters is sufficient revenues and a few years ahead. Moreover, and I must truly emphasize, these are all corrupt and ineffectively managed countries. None of them have even a reasonable institutional base, let alone a solid institutional base (that incorporated the rule of law, effective regulations, supervision and enforcement, rational economic policy formulation etc.) that is the foundation of sustained economic growth and prosperity.

L.S.: Has OPEC fears that the money parked in US treasuries (as part of the petrodollar recycling) might one day be wiped out? What would happen to the OPEC dollars being recycled if the banking system implodes? Are the Middle Eastern OPEC countries diversifying fast enough to escape the disaster that the Chinese are trying to escape from?

H.A.: Only a few OPEC countries have significant foreign assets–Qatar, the UAE (Abu Dhabi), Kuwait and Saudi Arabia. And of these, all have diversified except Saudi Arabia.

But as important is the fact that in all of these four countries, with the exception of Kuwait, the rulers behave as if these investments were in the first place theirs and they were sharing it with the general citizenry.

L.S.: Has anyone within OPEC ever thought about it that the White Man might have considered this all along: we get the oil, we give paper money, they park it with us, and some day when it becomes opportune we will eradicate the financial holdings on some dodgy pretext?

H.A.: I think that they used to in the late 1970s and early 1980s. But not since. The rulers want to stay in power and they need Western backing. This is first and foremost in their minds.

L.S.: Do you believe – like I do – that the time will come when oil-producing countries and other natural resource exporters will no longer sell their commodities for paper money like in the past but predominantly for hard assets such as precious metals – which would equal in my view “value gets exchanged for value”? And aren’t there actually signs for it? (2)

H.A.: Maybe, but only if they become independent countries with elected rulers, answerable governments and the rule of law. They have too much invested in the dollar to abandon it. Also, only a few of the exporters will continue to have current account surpluses and making it less important to have a currency or a commodity that maintains its purchasing power over time; because they will be spending it as they receive it.

The only signs of it are that all countries, not just oil exporters, have diversified their foreign exchange reserves into gold, and Iran because of sanctions is getting gold for some of its oil exports.

L.S.: But would you say it would make sense in general?

H.A: It only makes sense if an exporter has a continuing current account surplus and if it is managing its net foreign assets to finance its expenditures in the future and if gold is one asset in its diversified portfolio. It still does not need to get paid in gold because it can always turn around and immediately buy gold with its dollars and euros.

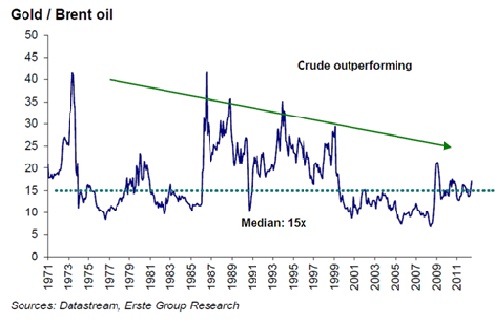

L.S.: What do you think about the fact that the oil-to-gold ratio has been remarkable stable for a long period? James G. Rickards for example told me once: “Of course the price of oil has moved between $30 per barrel and $150 per barrel, and the price of gold has moved between $200 an ounce and $1,500 an ounce, but if you look at the ratio, it always hovers around that 15-1 or 16-1 ratio, and that tells you something about the real intrinsic value of commodities.” (3) Take a look at this chart of the gold-oil ratio, please:

Your take?

H.A.: I believe that things tend to revert some sort of equilibria that change gradually with the passage of time, but no hard and fast rules. It may be in the range of 15-1 to 16-1 ratio but these ratios change with time and are not hard and fast. The ratio depends on long-term supply and demand developments.

L.S.: What do you think about the renaissance of gold in finance and banking in general? What does this tell you?

H.A.: Investors believe that central banks will do whatever to keep the party going.

L.S.: Since we were talking about oil prices, let’s talk about a related problem, let’s talk about Peak Oil. You say that Peak Oil is neither already upon us, nor will it be anytime soon. Why?

H.A.: As I said before, shale gas (and conventional gas) will be increasingly substituted for oil. Shale oil output will increase rapidly. I believe that Iraqi reserves will in time exceed that of Saudi Arabia. And if the Persian Gulf enjoys a number of years of peace, the countries could increase conventional oil output significantly above where it is today. So I see global oil output could increase significantly as needed, although at a higher price.

L.S.: So you think that the expanding world demand for crude oil can be matched in the next, say, twenty to thirty years?

H.A.: Absolutely.

L.S.: The country of which it is said that it has the most untapped oil reserves in the world is Iraq. Why is it that still very small portions of Iraqi oil reaches the global markets?

H.A.: I agree with your expectations but the problem is Iraq’s continuing political problems, its instability and the regional turmoil. I expect that the Shia-Sunni chasm to widen in Iraq and more broadly in the region (Bahrain, Saudi Arabia and Iran- Arab) and to become more explosive unless the West comes to its senses and does all it can to promote reconciliation.

If the region was stable, peaceful and with democratically elected governments, I am sure that foreign investment in the oil industry could become massive with a significant increase in the region’s oil and gas output.

L.S.: Is it any surprise to you that Chinese energy companies have a good standing in Iraq nowadays?

H.A.: Not at all. I believe not only in Iraq but this will become the case in Iran, too. And if China can close the deal with these two populous countries (with the US reducing its footprint in the region), it will become the oil power of the future.

L.S.: However, China is vulnerable when it comes to the transportation of the oil from that region. Don’t you think the US Navy has a say in that matter of China becoming the oil power of the future?

H.A.: Not really. China is quickly becoming the only Superpower on a par with the US (economically and militarily). If the US navy was to take any such action against Chinese interest, It would be akin to an act of war. I don’t believe that the US would interfere with the transportation of oil aboard Chinese vessels.

L.S.: A major problem related to oil is that most OPEC countries began in the 1980’s to exaggerate their reserves. What’s your opinion on this still persisting problem?

H.A.: I don’t think they are exaggerated today. I believe that there is much more oil in Iraq than currently estimated and also offshore in the waters of the Persian Gulf.

L.S.: How would you characterize the relations between Saudi Arabia and China on the one hand and the relations between Saudi Arabia and the United States on the other? In general, you think that the U.S.-Saudi alliance will end in tragedy for Washington. (4) Why so?

H.A.: China has been treading carefully in the region. It has not thrown its lot with Iran and Iraq for one very simple reason. It is not yet convinced that these two countries will be stable and prosperous in the near to medium term– to honor what they sign, to buy goods from China, etc. It still sees Saudi Arabia as the region’s oil giant because of the turmoil in Iraq and bad management in Iran.

I am absolutely sure that the US-Saudi deal that was cemented after WWII will end in tragedy unless the Al-Sauds and the US see the light. Let me explain.

The Saudi economic system is not sustainable. The Al-Sauds will not have enough revenues to afford subsidies for the general citizenry, without a thriving private sector, and with their massive military expenditures and revenues that they take for themselves.

A turnaround in Saudi Arabia will require massive political reforms (a deliberate transition towards a constitutional monarchy) and economic reforms (effective institutions, especially the rule of law, good regulatory, supervisory and enforcement policies, reduction of corruption, rational economic policies, etc.) that underly a thriving private sector that could deliver good paying jobs.

The Al-Sauds will not reform as long as the US will support them. It’s simple – the lust for power, control and human greed.

The US only reacts when it has no other options.

So the Al-Sauds and the US will go on as they have in the past. But eventually demostrations and armed conflict will come about. By then it will be too late!

L.S.: You’re an expert on Islamic finance. What are the merits of Islamic finance / banking? Is there true Islamic finance existing today?

H.A.: Islamic finance is all about risk sharing (equity and asset based) as opposed to risk shifting (debt based). It is thus a system that is naturally more stable.

Islamic banking is 100 percent reserve banking. This means banks have two functions. They keep deposits as cash, that is safekeeping. And they act as a mutual fund, that is they invest the money that people ask them to invest in assets of a particular risk class. They thus take no risk. Thus banks cannot become insolvent and panics and financial crises are avoided. Essentially such a system was proposed or endorsed by some of America’s greatest economists, including Irving Fisher and Milton Friedman, under what became to be known as the Chicago Plan. Recently, it has been also proposed under the heading of “limited purpose banking” by Professor Kotlikoff. But the financial industry and bankers don’t like such a system as it reduces their take.

No country in the world has an Islamic system. The country that is trying to move in that direction is Malaysia.

L.S.: What can (or maybe even should) the West learn from Islamic finance?

H.A.: The system as described above, at least for a banking system, is to my mind essential for restoring stability to our banking system. I don’t know how else it could be done as easily.

L.S.: Thank you very much for taking your time, Professor Askari!

H.A.: Thank you for having me.

For two and a half years Professor Askari served on the Executive Board of the International Monetary Fund and was Special Adviser to the Minister of Finance of Saudi Arabia; in this capacity he frequently spoke for Saudi Arabia at the IMF Executive Board. During 1990-1991 he was asked by the governments of Iran and Saudi Arabia to act as an intermediary to restore diplomatic relations; and in 1992 he was asked by the Emir of Kuwait to mediate with Iran.

He has advised ministers of finance, heads of central banks, oil ministers and other officials in the Persian Gulf. Furthermore, he has been a consultant to a number of multinational institutions and corporations, including: the OECD, the World Bank, the United Nations, the Gulf Cooperation Council, the Ministry of Finance of Saudi Arabia, the Ministry of Planning of Saudi Arabia, The US General Accounting Office, Bechtel, 1st National Bank of Chicago, Sunoco and ARCO International.

Sources:

(1) See for example Christian Stork: “The Complete Idiot’s Guide to Iran and the Bomb, Or: How I Learned to Stop Worrying and Love the Facts”, published at WhoWhatWhy.com on September 27, 2012 under: http://whowhatwhy.com/2012/09/27/the-complete-idiots-guide-to-iran-and-the-bomb-or-how-i-learned-to-stop-worrying-and-love-the-facts/, Christian Stork: “Iran Disinfo Watch: The AP Gets Thrown Another Curveball”, published at WhoWhatWhy on December 4, 2012 under: http://whowhatwhy.com/2012/12/04/iran-disinfo-watch-the-ap-gets-thrown-another-curveball/, and Pepe Escobar: “War fever as seen from Iran”, published at Asia Times Online on August 22, 2012 under: http://www.atimes.com/atimes/Middle_East/NH22Ak06.html

(2) See for example Robert Fisk: “The demise of the dollar”, published at The Independent on October 6, 2009 under: http://www.independent.co.uk/news/business/news/the-demise-of-the-dollar-1798175.html

(3) Lars Schall: “Germany should end the secrecy and bring its gold home”, published at Gata.org on October 10, 2011 under: http://www.gata.org/node/10550

(4) See Hossein Askari: “Saudi Arabia Sells Out Washington“, published at The National Interest on June 2, 2011 under: http://nationalinterest.org/commentary/false-friends-the-gulf-5393

Matterhorn Asset Management is dedicated to wealth preservation through safe and secure silver and gold storage in Switzerland. Protect your gold in the world’s safest vaults. To become a client, click here.

About Edward Maas

Edward Maas

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD