Distraction as Policy While Our Economic Rome Burns

Desperation and distraction are masquerading as economic policy. Below we see how and why—and at what cost.

COVID: The Great Economic and Political Hall-Pass

If every time I stole a cookie from the jar in front of my mom (age 8), or drove dad’s car (sometimes into a tree) without permission (age 16), failed a dorm-room inspection (age 17), broke a lawnmower for driving over a fence post (each year) or forgot a key anniversary (eh-hmm), it would have been so convenient to have a universal “hall pass” to excuse what is/was otherwise just plain stupid behavior.

Luckily for the grown children running our global financial system into the ground, the COVID pandemic is becoming precisely that: “A global hall pass for excusing decades of stupid.”

As we’ve written many times, inexcusably high debt levels, tanking growth data, struggling work force figures, embarrassing wealth disparity and insider market rigging between Wall Street and DC was well in play long before COVID made the headlines.

But now, the architects of such “pre-COVID stupid” have the current COVID narrative to justify and excuse even, well… more stupid.

The Latest Jobs Report “Explained” …

Take, for example, the latest job reports data from those DC-based creative writers at that comic-book publication otherwise known as the Bureau of Labor Statistics (BLS).

Known for years on Wall Street as mathematical magicians capable of turning 12% inflation into a 2% CPI lie, that same BLS is operating yet again to fib away the latest (and otherwise telling) jobs data.

The September jobs report was the second consecutive and disappointing report from the BLS, which they were quick to blame on “pandemic-related staffing fluctuations.”

Hmmm. That’s a nice phrase, no? “Pandemic-related staffing fluctuations.”

But the real description boils down to something more PRAVDA-like under the new Biden Vaccine Mandate, namely: “Obey or we take your job away.”

Needless to say, not everyone is obeying.

Since 2020, employment in local government education is down by 310,000; in state government education, employment is down by 194,000 jobs, and in private education the numbers are down by 172,000.

Ouch.

Why such “staffing fluctuations”?

The answer is simple: Many educated folks in the education sector don’t like being mandated to inject a vaccine into their bodies which by all reports from vaccinated infection rates, is no vaccine at all, but a debatable form of treatment at best.

Thankfully for all of us, I’m not interested in debating the hard vaccine data here, as folks like me should not be proffering unwanted medical expertise, which I clearly lack.

No one, myself included, really knows everything about mutating virology, but I’d wager to say that many of us are more mathematically dubious than Fauci is medically honest…

Jefferson (and History) Ignored

For followers of American history and markets, however, certain ideals and facts are easier to track despite distraction-as-policy tactics.

We are reminded, for example, of how passionately Thomas Jefferson warned us circa 1776 that a private central bank would eventually destroy our nation, and that only an educated population could save it.

Sadly, the new President is taking the inverse approach: Firing teachers and propping bankers.

Fast-forward some 240+ years from our founding fathers to our semi-conscious Biden, and we discover a nation wherein a private central bank effectively finances our national debt while the teachers, students and institutions charged with making citizens wiser, educated and free now find themselves locked out of their offices, classrooms and lecterns.

Seems a little upside down, no?

Red or blue, most of us can agree than nothing coming out of the White House in recent memory remotely resembles the vision or freedom-driven intellect of founding fathers like Jefferson, despite his known flaws.

Instead, we have seen red and blue administrations whose grasp on coherency, let alone math, history, economics or even Afghan geography is questionable at best.

Biden’s Response

And what does Biden (or his “advisors”) have to say about the recent and scary numbers within a gutted and “locked-out” educational labor force?

Well, you’ll have to see it to believe it.

Really? Really? Really?

That’s right folks.

The President of the United States, home to the world’s reserve currency and former beacon of global freedom, is telling Americans not to worry about the slow death of genuinely informed dissent (as well as educational access and jobs) or the attempted popularizing of otherwise tyrannical mandates, but to focus instead on the vaccine rates at United Airlines?

Yes. Really.

The leader of the free world is boastfully telling us that the “bigger story” is a fully vaccinated United Airlines (who were forced to choose between a jab or job), so why worry about the problems in that silly ol’ educational sector or outdated Bill of Rights?

Playing with Minnows While Ignoring Whales

Where ever one stands on the understandably divisive vaccine issue, how can anyone compare a private airline’s vaccine rate to a national education, civil liberty and employment crisis?

Why are politicians, Davos dragons, statisticians, media bobble-heads and central bankers focusing our/your attention more on a virus with a case fatality rate of less than 0.5% than they are on openly addressing whale-sized issues like unsustainable debt, rising inflation, embarrassing labor inequality, a dying currency or even more declining GDP?

Deliberate and Desperate Distraction as Policy

Well, history tells us why.

As anyone not banned from a classroom knows, the history of desperate leaders seeking to distract, censor and control the masses in times of a self-inflicted and debt-induced cycle of internal economic rot is long and distinguished.

As Biden doubles down on the bad (yet deliberately distracting) hand of what was hoped to be an optically humanitarian policy of vaccine mandates, the masses are getting restless as well as fired…

Solution?

Criminalize the non-consenting as anti-vaccine, anti-science or anti-American “flat-earthers” while denying open discussion on such otherwise relevant topics as basic math, constitutional law, calm science or individual rights…

Meanwhile, those who won’t tow Biden’s increasingly incoherent mandate (or Don Lemmon’s always coherent ignorance) are losing jobs and/or forced to prioritize (in a Jeffersonian way) individual liberty over financial security.

Ben Franklin, of course, said those who surrender liberties for security deserve neither.

In such a polarized backdrop, everyone, pro or anti-vaccine, loses.

Informed, open and calm debate has been replaced by a contradictory, censored, sanctimonious and hysterical autocracy from prompt-readers to political puppets.

So much for leading the free world… Let me remind Biden to consider the words of another founding father, Thomas Paine:

“I have always strenuously supported the right of every man to his own opinion, however different that opinion might be to mine. He who denies to another this right, makes a slave of himself to his present opinion, because he precludes himself the right of changing it.”

As someone who studied and practiced constitutional law, worked within a rigged Wall Street and read nearly every book I could find on America’s founding fathers, I can say without hyperbole that I no longer recognize the country (or values) of my birth nation.

As Franklin also noted, “All democracies eventually die; usually by suicide.”

Hmmm.

But let’s get off my high-horse and back to those job reports…

Conviction vs. Employment

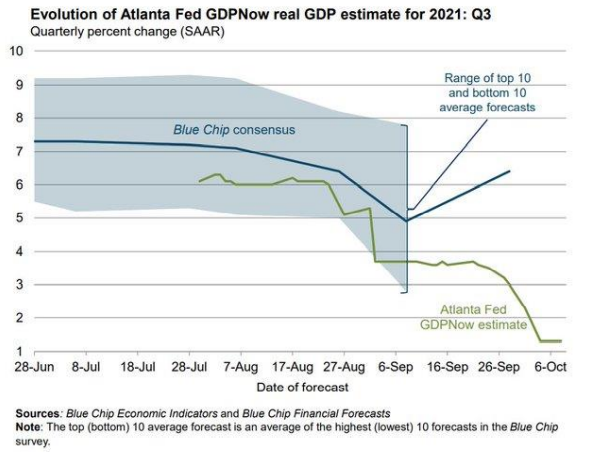

As Bloomberg recently noted, the result of these “pandemic-related staffing fluctuations” is a bit alarming.

The following critical industries are witnessing the following job-loss percentages: Nursing and Residential Care (-1.26%); Local Government Education (-1.83%); Community Care for the Elderly (-2.20%) and lodging (-2.25%).

But thank goodness that despite a deliberate weaning of nurses, teachers and elderly care experts, United Airlines is nearly fully vaccinated and our Motion Picture Industry (universally known for its astounding political and financial wisdom) is seeing a +4.21% job increase.

Awe, but as Johny Mellencamp would say, “Aint that America?”

Now instead of more employed and free-thinking nurses, teachers and students allowed to gather, speak and think freely at their own campus or clinic, we can be glad that jobs in Hollywood, like DC, are growing to keep us living on more fantasy rather than actual, informed and hard-earned knowledge.

Oh, and the Economy…

But rather than just rant otherwise rhetorical sarcasm, let’s get back to those other barbaric (and soon-to-be empty) old-school disciplines like economics…

Biden’s mandates are more than just evidence of distraction as policy and constitutional interpretation/usurpation, they have direct impacts on our financial lives outside of the deliberately exaggerated vaccine debacle/debate.

Let’s go down the list of what economics taught us years ago, when we were allowed to enter a classroom:

- Stagflation Ahead.

As more and more folks are locked out of work, the entitlement costs for these “un-American” free-thinkers will rise, placing greater inflationary pressures upon a deliberately constrained rather than open economy.

Rising inflation + slowing economic activity = stagflation.

Prepare for this, as that’s what’s coming.

Inflation, by the way, is an invisible tax on those who can afford it the least. Thanks again Powell et al for shafting the middle class…

- A Divided States of America

A country which once revered open rather than censored debate, investigative rather than complicit journalism, and respected rather than polarized differences of opinion, is becoming increasingly factionalized, divided and angry.

Jab or no jab, I fully respect both views. Can’t we all do the same without a “mandate”?

Like Thomas Paine, I hope so, because as Thomas Jefferson warned, we face far greater economic and political threats ahead than COVID.

Rather than accountability, transparency and cooperation, leadership today is defined by fantasy and magic, from magical money created at the Fed to magical employment and CPI data downplayed at the BLS.

Such left or right fantasy-as-policy is as old as history—it’s darker side, that is. Just ask Lenin, Castro, Nixon or Greenspan.

Whenever backed into a debt corner of their own design, leaders employ a familiar combo of boogeyman and salvation narratives to divert the masses away from the slow-drip erosion of their personal liberties, dying currencies and debt-driven stagnation.

This distraction-as-policy is happening right now. The rise of the COVID narrative in 2020 is more than a coincidence. It’s a conveniently exploited opportunity for political and financial opportunists.

- More Centralized Controls and Fake Markets

With debt levels far beyond the Pale of productivity levels (i.e., embarrassing debt to GDP ratios), the U.S. and other developed economies are mathematically and factually unable to ever grow their way out of the debt hole they have been digging us into for years.

Period. Full stop.

If I know this, and if you know this, well…they certainly know this too in DC.

The only difference is that these policy makers, like most kids caught with a hand in the cookie jar, are incapable of admitting fault.

Instead, today’s “leadership” can blame their economic and policy failures (and self-preservation rather than “service” instincts) on something else—i.e., “COVID did it.”

But as we’ve voiced elsewhere, the debt time bomb, growth declines, social unrest, wealth disparity and failing political credibilities in play today were already a major problem BEFORE COVID.

Now, as then, the empirical data objectively confirms that tanking manufacturing data, jobs growth, economic productivity, broken supply chains, scary transport numbers and political mistrust can never service the over $28.5T in public debt sitting on Uncle Sam’s bar-tab.

As a natural result, we can therefore expect far more “accommodation” (i.e., monetary expansion) from the Fed, and far more “Fiscal Stimulus” (i.e., deficit spending) from our comical legislature ahead.

Stated otherwise: Get ready for more real debt, fake money, centralized controls and hidden wealth destruction.

Zombie Stocks, Bonds and Bankers: Too Big to Fail 2.0

Sadly, one of the only forms of income which Uncle Sam enjoys today is the capital gains receipts from a bloated, rigged and artificially Fed-supported stock market.

This means we can anticipate more “stimulus” for a zombie, crack-up-boomed market well past its natural expiration date.

The same is true of for government IOU’s. No one wants our bonds. 2020 saw $500B in foreign outflows rather than inflows for US Treasuries.

So, who will pay Uncle Sam’s bar tab now?

Easy: Uncle Fed at the Eccles Building down the avenue from a Treasury Department now led by a former Fed Chairwoman.

One really can’t make this crazy up. It’s all that real, that rigged and that true.

The U.S. debt crisis is now being “solved” by a circular loop of a Wall Street and a White House children tossing their hot potatoes of bad debt (MBS and sovereign) around until they are bought with money created out of thin air by the Fed.

And yet despite such insider support, rigged markets and “accommodated” securities, even the rising tax receipts from these bloated markets are not enough to cover the interest expense on Uncle Sam’s bar tab.

In short, US Treasury bonds and stocks are openly supported Frankenstein-assets kept alive by a central bank and White House cabal (sorry, Mr. Jefferson…) who blame every problem (and justify every expenditure) on a virus rather than confess to the cancerous reality of over 20+ years of their open and obvious mismanagement of a rigged banking and distorted financial system.

But rather than account for such sins, we can expect a bigger bail-out rather than an honest confession…

In 2008, for example, the response from DC and NYC to bankers gone mad was to declare bankrupt banks as “Too Big to Fail.”

Fast-forward some 13 years later and that same toxic duo of bankers and politicos have now effectively telegraphed that bankrupt government bonds and private stocks are also “too big to fail.”

That ought to anger an informed population. But instead, we are fighting about masks, vaccine shaming and Prince Harry’s sensitive upbringing.

So far, the distraction-as-policy technique seems to be working in favor of the foxes guarding our financial henhouse.

Signal More Currency-Debasing “Miracle Solutions”

Which brings us right back to a harsh but increasingly undeniable yet ironic reality.

If objectively broken bonds, stocks and financial regimes are too big to fail, then the only way to “save” them is with more mouse-click-created currencies which are too debased to succeed.

As precious metal and other long-term, real-asset investors long ago understood, currency expansion is just another name for currency debasement.

In other words, eventually, all that “system saving” new money simply drowns the system it was allegedly designed to save in ever more debased dollars.

Again, it’s just that tragic and just that simple.

Yes: More monetary and debt expansion can buy time and rising markets.

But those markets are measured in currencies which time has equally taught us lose their value with each passing second.

And the only ones paying for that time are you and I–with dollars, euros, yen and pesos whose purchasing power and inherent value are tanking faster than the credibility of the folks who brought us to this historical and debt-driven turning point.

Stated bluntly: The financial and political leadership of the last 20+ years has placed the global financial system into a debt corner for which there is no exit other than deliberate inflation (and hence currency debasement).

This foreseeable disaster, however, is now conveniently blamed on a current pandemic rather than a grotesque history of equally grotesque mismanagement by policy markets who have confused debt with prosperity and double-speak with accountability.

Wouldn’t it be nice if such economic topics were making at least as many headlines as the latest infection rates?

Meanwhile, the mainstream media pursues plays chess with context-empty headlines, bogus job data and ignored debt bombs as our economic Rome (and currencies) burns silently around us all.

About Matthew Piepenburg

Matthew Piepenburg

Partner

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD