“Transitory” Inflation? — Sublime Yet Ridiculous

History is a funny thing, almost as funny as human nature. The policy makers, including their latest meme of “transitory inflation,” are no exception to such psychological tragi-comedy.

In short, we don’t see inflation as “transitory.”

Transitory Hope, Timeless Lies

It’s sometimes helpful to step outside of market history to gain perspective on human behavior, and hence, measure leadership trends at other desperate turning points similar to the one markets are now careening toward.

By late 1864, for example, as Union forces under General Grant bore closer to Richmond at the tail-end of a long and passionate civil war which a grossly outnumbered Confederate Army was (by then) destined to lose, hope nevertheless sprung eternal from an increasingly discredited leadership.

Jefferson Davis, President of the Confederate States, described the mounting casualties, dying currency and withering food supplies as only “transitory.”

Less than 100 years later, as the German Wehrmacht lost its 6th Army to the cold winter and red-hot resistance of the Red Army, the propaganda machine in Berlin described that war-ending turning point in 1943 as merely a “temporary setback.”

Speaking of dying armies, Napoleon’s 1812 march into Russia with 360,000 soldiers ended in disaster when he marched out with just under 15,000 soldiers left, prompting the infamous (and shivering) Bonaparte to declare, “It’s only a small step from the sublime to the ridiculous.”

Transitory Inflation: More Fantasies from On High

Fast-forward to the Fed’s current war against natural market forces and we see yet another ridiculous example of a losing war whose inflationary death toll is being otherwise touted by our financial leadership as “transitory” or “temporary.”

Like the foregoing military examples, market bulls, sell-siders, politicians and central bankers share an uncanny capacity to ignore the obvious and promote the fantastical—as fantasy is often easier to bear (and sell to the masses) than reality.

Fantasy, after all, is as effective a tool for re-lection, Fed-tenure and advisory fees in a losing market war as it is a patriotic weapon in a losing military war.

The most recent example of fantasy as policy is now evident in the popular meme that the +4% year-on-year inflation numbers in April and May are merely “transitory.”

In short, we are now being told not to worry about inflation.

That is, we can all calm down, for inflation, we are asked to believe, is as “temporary” today as the year 1-year cap on QE we were promised from Bernanke as far back as 2009, when the Fed’s balance sheet was under $1T rather than the current $7+T.

So much for promises of the “temporary” …

As for inflation being anything but “transitory,” we’ve given countless warnings, proofs and solutions to current and increasing inflation to come.

Like Robert E. Lee’s outnumbered army, the math makes future of inflation, and the slow death of the dollar, inevitable rather than theoretical.

And yet now more than ever there are those telling us not to worry about inflation or its implications.

Defending the Dis-Inflationary

In fact, and in all fairness to those who feel deflation rather than inflation is ahead, we’ve given fair voice to their viewsas well.

Nevertheless, and sadly, it seems necessary, yet again, to return to history, economic Real Politik and math to help the inflationary truth sink in.

That is, it’s time to fact-check the hope-peddlers so common to the main stream financial propaganda that surrounds us today as markets move from the Fed-supported sublime to the inflationary ridiculous.

In all fairness to the great inflation vs. deflation debate (or war), there are, again, fair arguments to be made against inflation as a long-term reality.

The latest and most common arguments against current inflation include the popular belief that supply-chain disruptions on everything from lumber to computer chips are only “temporary.”

Once these “transitory” disruptions are resolved, supply will recover and inflationary forces will vanish.

Fair enough.

Another argument gaining bullish momentum against inflation is blaming the “temporary” climb in the CPI measure of inflation on rising car prices.

Fair enough.

Deflationary pundits will also remind us that inflation numbers are un-naturally high because they measure rising prices in silly little things like food and energy. Thus, if you take them out of the equation, then inflation is really closer to 2%, so why panic?

Then again, if you have a report card with 3 A’s and 2 F’s, that too is not a problem if you simply disregard the 2 F’s… Besides, who needs food or energy anyway?

Deflationists (as well MMT fantasy pushers) will further remind that even the extreme monetary expansion unleashed by central bank money printers is not inflationary, as all that printed money never hits “velocity speed” in the real economy, and thus has no inflationary impact.

Fair enough.

Finally, the pro-deflationist camp will rightfully remind us that massive debt levels, decades of Uncle Sam’s ability to export inflation overseas and the slow economic growth of the pandemic economy will cool demand and keep prices low rather than high—all anti-inflationary forces.

Fair enough.

But here’s the rub: “Fair enough” is not the same as “true enough,” and whether one chooses to believe it or not, inflation is not only coming, it’s already here and it isn’t going to be “transitory.”

Inflation: Anything but “Transitory”

Ok, so how can we be so certain in a world of uncertainty?

Well, for one thing, the very CPI scale used to measure inflation is the open joke on Wall Street, and measures inflation about as well as Lance Armstrong’s lie detector measures truth.

We’ve addressed this topic ad nauseum.

Thus, dis-inflationary pundits can defend all day long the “transitory” nature of rising prices on everything from computer chips to used trucks, but they are ignoring the larger fact of defending their non-inflationary case with a discredited CPI witness…

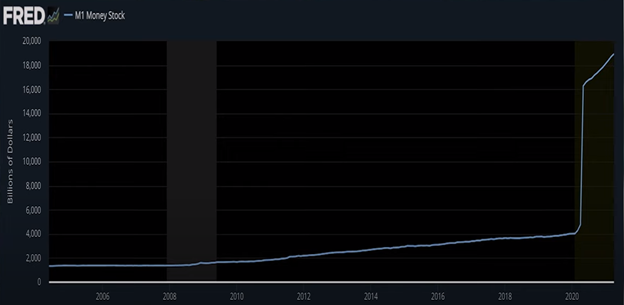

Adding to the inflationary reality which is anything but “transitory” is the very definition of inflation itself, which hinges less upon that bogus CPI scale and far more upon a single metric: Increases in the broad money supply.

In case such an evidentiary (as well as mathematically obvious) increase doesn’t give you an inflationary chill, just consider the following increase in the M1 money supply. A picture, after all, says 1000 words (or billions) …

Furthermore, even if one discredits money printing (i.e., monetary policy) as inflationary due to the lack of “velocity” of printed dollars trapped behind the Hoover-like dam of the Fed, Treasury Department and TBTF banks, one simply can’t deny the inflationary effects of fiscal policy—that is: money pouring directly (and at increasing velocity) into the real economy.

Biden, for example, is proposing a $6T budget to Congress. Will it pass? Or will it be watered down to a meager $5.5T or $4.8T?

But what’s a trillion here or a trillion there in this surreal new abnormal? Given all the money spewing out of DC, trillions have become banalized to mean almost nothing to a nation and market addicted to fake money.

Then again, we all know how addictions end: You either quit or die.

Furthermore, and quite telling, is the simple fact that the Fed itself favors inflation, as there’s no better way to get themselves out of a $30T public debt hole of their own digging than by sucker-punching the masses with deliberate inflation to pay off their own debt binge with increasingly inflation-debased dollars.

The FOMC, like any general staff in a losing war, will pretend that such a currency casualty is “transitory,” or that they otherwise have the “temporary inflation battle” under control.

The Fed calls their battle plan “symmetrical inflationary targeting,” pretending to the world that they can order inflation around like a cadet at West Point.

But then again, if the Fed controls the very scale that measures inflation, perhaps they can keep bluffing (lying) their way around otherwise obvious inflation a bit longer. Either way, the end result is unavoidable.

But think about that for a second: The Fed measuring its own inflationary policy is like the Wuhan Lab measuring its own viral leaks…

An Ode to Fed Apologists

Fed apologists/cheerleaders, however, will continue with their fantasy defense that the Fed will eventually “tackle” the inflationary problem once they have full confirmation that it’s running too hot.

We discussed the open dishonesty as well as mathematical impossibility of the Fed tackling the debt (and hence inflation) problem “down the road” in a recorded interview here.

Despite such contrary math, the cheerleaders tell us the Fed will eventually step in with some needed “tapering” to keep inflation under control.

Furthermore, the Fed itself will make even more comical claims that they are very worried about unemployment, and that if jobs reports (and non-farm payrolls) continue to disappoint, the FOMC superheroes will need to keep printing money to buy bonds and keep rates low.

After all, the Fed was created to help the little guy, right? The Fed’s entire mission is to keep employment strong, right?

Well, if you believe that, do a little more research on who created the Fed and why…

The Fed’s Real Mandate: Faking It

But even if historical research on the Fed’s true origins and mission are of no interest, then just stick to current math and basic realism.

As I’ve written so many times elsewhere, the Fed is not holding back its “tapering” option just to help improve employment.

Nope.

Instead, the Fed is going to hold back tapering because they have taken our nation to the highest levels of debt danger ever seen in its history; thus, if they were to ever “taper” and allow rates to naturally rise, Uncle Sam (and the markets) would be insolvent faster than Powell can mince words on 60 Minutes.

In short, “tapering” is not an option, it’s a fantasy buzz-word for troops otherwise losing morale.

This means the money printers will continue to run hot to the tune of billions per month and deficit spending (along with Fed balance sheets) will continue run hot to the tune of trillions per year, which means inflation is and will be anything but “transitory.”

Does this mean that the year-over-year rate of change in inflation will be 4%, then 5% then 6% with each passing month on a never-ending rise to the north?

No.

Inflation numbers, including the fictional ones coming out of DC, will see peaks and valleys, and I’m not suggesting inflation will hit 18% by the time you read this.

Nor am I suggesting that periods of disinflationary “relief” won’t make the headlines soon if, for example, lumber and car prices revert to their means, which is always possible, if not likely, once bottlenecks at saw mills and shipping ports are reduced.

And hey, maybe Fauci et all will be able to lock us all down with ever-knew COVID variant headlines which crush demand and alas, dis-inflate the CPI.

Again, nothing moves in a straight line, including inflation, but the trends and realities (monetary and fiscal excess) discussed above are not “transitory” and thus neither is (or will be) inflation.

Of course, inflation is a deadly enemy. It eats away at market returns, savings accounts, currency power and hence spending power.

Like the winter outside of Moscow, Borodino, Petersburg or Stalingrad, it’s a silent killer.

And like Napoleon’s army in Russia or Lee at Gettysburg, our financial leaders now stand before a cannonade of fatal money supply levels and yet still think (or tell us) they are winning…

In short, they have already taken our markets, economies and currencies over that fine line from the sublime to the ridiculous.

But like many of their faithful soldiers and current investors, those with the most to lose just don’t know the danger they are already in or the war their currencies will inevitably lose.

That’s neither sublime nor ridiculous; just tragic.

About Matthew Piepenburg

Matthew Piepenburg

Partner

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD